- Proverbs & Profits

- Posts

- Dave Ramsey Hates All Debt - Should You?

Dave Ramsey Hates All Debt - Should You?

Zach Nelson

May 30, 2024

Dave Ramsey Hates All Debt - Should You?

Read time: 6 minutes

If you’ve been trying to learn about money for more than 5 minutes, you’ve heard of Dave Ramsey.

And the first thing you realize about Dave, is “Wow, this guy really hates debt.”

He despises credit cards, even when paid off in full each month.

He never takes on a car payment.

He is against all student loans.

And he will never buy a house with a mortgage. Cash only.

And he’s even got a Bible verse to back himself up.

The rich rule over the poor, and the borrower is slave to the lender.

Dave claims the quickest way to freedom is to be 100% debt free. Anything less is slowing you down and asking for trouble.

Yet critics say he’s too strict and his plan actually LOWERS your ability to build wealth.

Who’s right?

Is it best to avoid all debt?

Or is it possible to use debt wisely?

Let’s talk about it.

In today’s issue:

What the Bible says about debt

Is all debt the same?

The great debate! Debt - Hazardous or Helpful?

Forwarded this email? Subscribe here

What does the Bible say?

Let’s first make it clear that the Bible does NOT forbid taking on debt.

Nowhere in scripture is there a ban on borrowing money.

The closest we get to a ban is Dave Ramsey’s most quoted verse:

The rich rule over the poor, and the borrower is slave to the lender.

Pretty strong language, but what does this actually mean?

When you sign on the dotted line for a loan, you have now promised your future income (paychecks) to that lender.

Those paychecks represent your future time.

So by taking on a loan - any loan - you are trading your future time working to pay that lender back in exchange for whatever you’re buying now.

That lender now owns your time.

The way Proverbs phrases it, you are now a slave to that lender.

That's a strong warning, but it’s not an outright ban.

More like, “buyer beware”.

Even Dave Ramsey himself admits this, as he allows people to take out mortgages to buy homes, even though he personally refuses to.

“Okay, so you’re not going to burn in hell for financing your car. That doesn’t mean Dave Ramsey is wrong about avoiding all debt.”

Very true. He may still be right, avoiding being a slave seems like a good idea.

Let's take a look at another scripture passage.

Then he said, “Go outside, borrow vessels from all your neighbors, empty vessels and not too few.

In this passage, a widow has just lost her husband, and the family is in deep debt.

Faced with losing her two sons to slavery to pay back the lender, she turns to the prophet Elisha for help.

What does he tell her? Go, borrow as many containers as you can.

Those containers are then miraculously filled with oil, which she sells to pay back her debts and have money to live on.

Two chapters later, we see hints of the same concept. Elisha and his prophets had outgrown their meeting space.

To fix this, a group of his homeboys go down to the Jordan to build a new building.

As they're cutting lumber for the new space, one of the ax heads falls off its handle and into the river.

The prophet is upset, because it was an expensive tool and he had borrowed it for the work.

Rather than lecturing him about debt, Elisha caused the ax to float to the surface of the river where he could retrieve it.

So what’s similar about these two stories?

Well, other than having a legendary prophet on hand to get themselves out of a pickle, these stories both show people borrowing and using “debt” (or something similar) to be more productive.

In other words, the debt they took on was to build or to earn a better income.

I like to call this type of debt, productive debt.

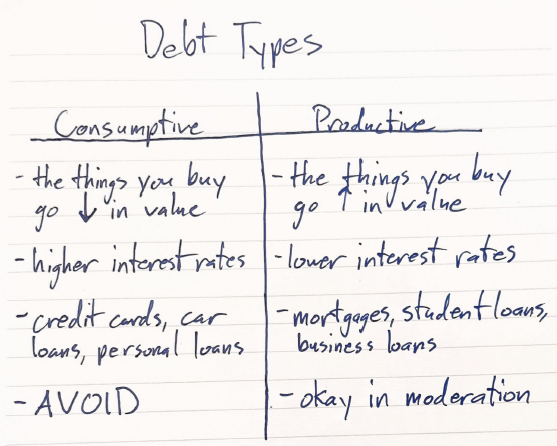

Types of Debt

There are two main types of debt - consumptive debt and productive debt.

Consumptive debt is used to buy anything that you consume or that goes down in value over time.

Think credit cards, car loans, personal loans, or time shares.

This type of debt usually has high interest rates, and the item you’re buying does not increase your net worth.

Productive debt is used to buy things that go up in value or help you increase your net worth.

Think mortgages, student loans, and business loans.

This type of debt usually has lower interest rates (though not always), and what you buy with it usually will increase your net worth over time.

Because those items go up in value over time or help you earn a higher income, using the debt can help you grow your wealth.

Unfortunately, it’s still debt. And it also increases your risk of losing everything by having it.

It’s useful, but it’s also dangerous, like a sharp knife.

The great debate! Debt - Hazardous or Helpful?

99% of financial experts agree with Dave on this - avoid consumptive debt like the plague.

Nothing will keep you poor like borrowing money to buy things that go down in value.

This goes for vacations, eating out, shopping, and, yes, even cars.

I don’t care if it’s a 50% interest rate or a 0% interest rate, buying consumptive things with loans causes you to overspend and steals your ability to build wealth.

If you don’t have the cash to pay for it now, don’t buy it until you do.

But productive debt is where the conversation gets interesting.

Dave Ramsey is adamantly against this type of debt too.

My freshman year of college was going to cost me $6,000 out of pocket after scholarships and grants.

At my current job I was earning $9/hour, or $18,000 per year. After graduation, I’d be making $60k.

Dave would have told me to work hard for a year or two to save up for college and avoid taking on the debt.

Ignoring the fact that I would have lost my scholarships by doing this, by delaying my post-college career by even a year, I’d be losing out on $42,000 of earnings.

It doesn’t take a math degree to see that in this case, taking on the student loans could be a great financial move.

Similarly, Dave tells people to never have a mortgage on an investment property.

If you want to buy a single family home to rent out, he says you’ve got to save up the $375k in cash to buy it outright.

Let’s be honest, for most people that could take a decade or more. Meanwhile, you’re losing out on years of growth and rent payments.

It’s super-ultra safe, but also super-ultra slow.

What if instead you put 20% down and got a traditional 30-year mortgage?

That's much more approachable. And actually possible.

Yes, buying property with any kind of debt increases your risk of losing everything, but a vanilla loan like that is not what gets most people into trouble.

It's plain and boring and doesn’t put you in a position where everything needs to go right for you to succeed.

Remember, we’re not using debt to buy something we’ll consume, we’re using it to buy something that will pay us cashflow and go up in value over time. It’s a big difference.

However, some people will try to use as much debt as possible when investing.

They want to grow fast, fast fast!

If that’s what you are trying to do, I agree with Dave, that's a terrible idea.

You might grow fast, but a few bad breaks can ruin you when you load up on debt.

It’s like seeing how great a kitchen knife is, then filling every square inch of your kitchen with knives so you can chop things as fast as possible.

Sooner or later you’re going to get cut.

That used to be Dave Ramsey, actually.

He first became a millionaire using fancy loans to buy and flip real estate.

It was the debt equivalent of juggling knives over his head blindfolded.

He was good at it, until, out of nowhere, the bank messed with the knives.

He lost everything.

But Dave’s response to getting cut has been to ban all knives from the kitchen forever.

That’s an overreaction.

The correct answer isn't that all knives are bad, it's to not juggle the stinking knives!

Where does that leave us?

I agree with Dave - most of the time.

But I also believe that at times, debt can be a useful tool.

It can help you buy a home, it can help you get an education, it can help you buy a business - all things that help you earn more than the debt will cost you.

Like a knife, treat it with respect - don’t start swinging it at everything.

But learning how and when to use it can be a huge help when building wealth.

Over the next few weeks we’re going to be diving into all things debt.

When to use it and how

How to pay it off as fast as possible

How to balance paying off debt with investing and buying a home

And which type of debt I hate more than any other

If you'd like to come along for the ride, make sure you’re subscribed so you don’t miss out.

See you next week!

Keep growing,

What’d you think of this week’s newsletter? Hit reply to let me know!

Forwarded this email? Subscribe here