- Proverbs & Profits

- Posts

- 9 Smart Money Moves to Make Before the End of the Year

9 Smart Money Moves to Make Before the End of the Year

Zach Nelson

December 17, 2024

9 Smart Money Moves to Make Before the End of the Year

As the year comes to a close, you have two choices…

Settle in for a comfy 2 weeks, then figure out your money in the new year

Take action today and set yourself up in 2025 to see your biggest growth yet

If you are person #1, more power to you.

Go turn on some Christmas music and do something else, I’ll see you in January.

For everyone else, I spent 20 hours finding the best year-end money moves you can make so you can thrive in 2025. (hey that rhymes)

And half of them no one is talking about.

In today’s issue:

New segment from the readers!

9 tactical money moves that have BIG payoffs later

Forwarded this email? Subscribe here

New Segment, The Mailbox - Featuring You!

After every newsletter, I get a flurry of responses with great insights that build on the original article.

Most weeks, at least one of your emails will make me think, “Man! I wish I had included that when I wrote it!”

Well, today we’re going to experiment with just that.

Below is a response I received to last week’s newsletter.

(Click here to read it if you missed it)

“Great article to stimulate thinking. It truly shows how small, consistent changes that result in cost savings can make a huge difference in the long term, IF invested in an index fund.

That of course is a big IF.

Many people don't think of investing that savings; especially if it is small and seemingly insignificant.

One other thought - the example you used of walking a mile each way to get groceries would probably seem extreme to most people.

A working parent with 2 kids isn't going to walk to and from the grocery store 4 times a week. But the principle of small savings adding up over time is sound.

What is the result of packing a lunch even just 1 day a week?

How about giving up one Starbucks a week and investing the $5+ saved?”

-Sean

You’re right, without the investing component, this plan isn’t very lucrative.

The total amount saved over the years is only $17,275.

The rest is the growth of the investments. ($280,000 of it!)

If you never invest, you can save like Scrooge himself and never build wealth.

But don’t let that stop you - investing is easy.

Let me show you how it works for me…

I don’t actually keep track of the money I save each time I walk and don’t drive my car.

Instead, once I find some savings in my budget, I increase my automatic monthly investing transfer.

The investing now happens on repeat forever without me ever thinking about it again.

The more I do this, the larger the stream of savings becomes, until it’s an unstoppable tidal wave of money flooding my investment account.

Find some savings and see for yourself

Pack a lunch to work

Replace one Uber Eats meal with a frozen pizza

Give up Starbucks

And watch your net worth grow.

I put together a quick table to show you the impact those savings can have on your finances.

Wild, isn’t it?

Don’t ever believe that small actions aren’t powerful.

Thanks for the message, Sean.

If you’d like to join in the conversation (and maybe get featured yourself!), just hit reply to any newsletter with your thoughts on the topic.

I read every reply, and you might even get super-micro internet famous.

Onto this week’s article….

9 smart money moves before the year ends to save more, give smarter, and get ahead

Basic

1. Contribute to a Roth IRA

A Roth IRA is the best place to save for retirement.

Normally when you invest, if that investment makes you any money, the government wants a piece of it.

Did your stock just pay you dividends? Here comes the IRS - “Taxes please.”

Rental property pay you rent? - “Taxes pleeeease!”

Sell your Amazon stock for a huge gain? - “Thank you very much for your taxes pleaseeee! 🙃*”

Not in a Roth IRA.

Any money your investment makes for you is tax-free. For life.

And all you have to do is promise not to spend it before you retire. (technically age 59 ½)

That’s what we call a good freaking deal.

*Side note - maybe taxes wouldn’t hurt as much if the IRS started including emojis on your tax bill.

If you can throw some extra cash together before the end of the year, get started. It’s easy to set up.

What to know: Contributions are capped at $6,500 for 2024 ($7,500 if age 50+), with income limits for who can contribute.

How to Start: Most banks offer a Roth IRA account. Some of the most common providers are Vanguard, Fidelity, and Charles Schwab.

Pro tip: Don’t forget to choose something to invest in once you contribute your money to the Roth IRA.

If you leave it uninvested once it’s in the account, you don’t get those sweet tax savings on the growth! I personally use an S&P500 index fund to keep it simple.

2. Make a Budget for January

I get why you don’t have a budget yet.

It’s scary.

It’s boring.

And it’s… actually, it’s not any of those things. Budgets are awesome!

Budgets kick butt, take names, and make you look like Brad Pitt.**

Your life is too short to wing it with your money, especially when you can build a budget in less than an hour.

It will be wrong.

It will be gross.

But it will be yours.

And you will finally be telling your money what to do, instead of your money telling you what to do.

How to Do It:

Download any budget template you like the look of (reply to this email if you want a copy of mine)

Fill in your income

Estimate your expenses for January

Test it out. On January 31st, see what worked and what didn’t, and make a new one for February.

Rinse and repeat, all the way to freedom.

**If you squint hard enough.

3. Open a High-Yield Savings Account (HYSA)

Every person needs a savings account that’s separate from their checking account.

This is where you hold your emergency fund and park short-term savings (like buying a home).

I have several, each with its own savings goal.

Putting your money in a separate account reduces your urge to spend it when youyour checking account is flush with money.

And a HYSA earns you much higher interest rates than traditional savings accounts so your savings grow faster.

Why Do It: HYSAs are perfect for emergency funds or short-term savings, offering rates 10–15 times higher than standard accounts.

Top Providers: Consider banks like Ally, Marcus by Goldman Sachs, or CapitalOne 360.

Pro Tip: Look for accounts with no fees or minimum balances.

*I’m not affiliated with any of the companies mentioned in this article and don’t make a dime if you click any of the links.

Intermediate

4. Check Your Credit Reports for Free

You need to know what’s in your credit report.

You will catch mistakes (they happen all the time)

You will catch fraud if someone’s using your identity to take out loans

You will see forgotten debts that are secretly destroying your credit score

Every American gets 1 free credit report review per year from each credit reporting agency (there are 3).

If you like, you can pull all 3 at once, or pull one every 4 months to keep tabs on things more often.

It’s super easy to do. Probably takes 15 minutes apiece.

How to Do It:

Visit AnnualCreditReport.com for free access to your credit reports from Experian, TransUnion, and Equifax.

Look for incorrect personal information, unfamiliar accounts, or outdated records.

Why It’s Important: Your credit report affects things like

Loan approvals

Interest rates

Rental applications

Job opportunities

5. Contribute to a 529 Plan

A 529 plan is a savings account for college that lets you take a tax deduction on your contributions.

On top of that, money in the account can be invested and grow tax-free.

That makes a 529 account the most powerful tool for saving for college.

Contributing before January will let you take those tax deductions in 2024.

If you think you or your child will need money for college, take a look at it before the year ends.

Why Do It Now: Contributions may qualify for state tax deductions or credits, and starting early maximizes compounding growth.

How to Start: Check out plans at Saving for College or through your state’s website.

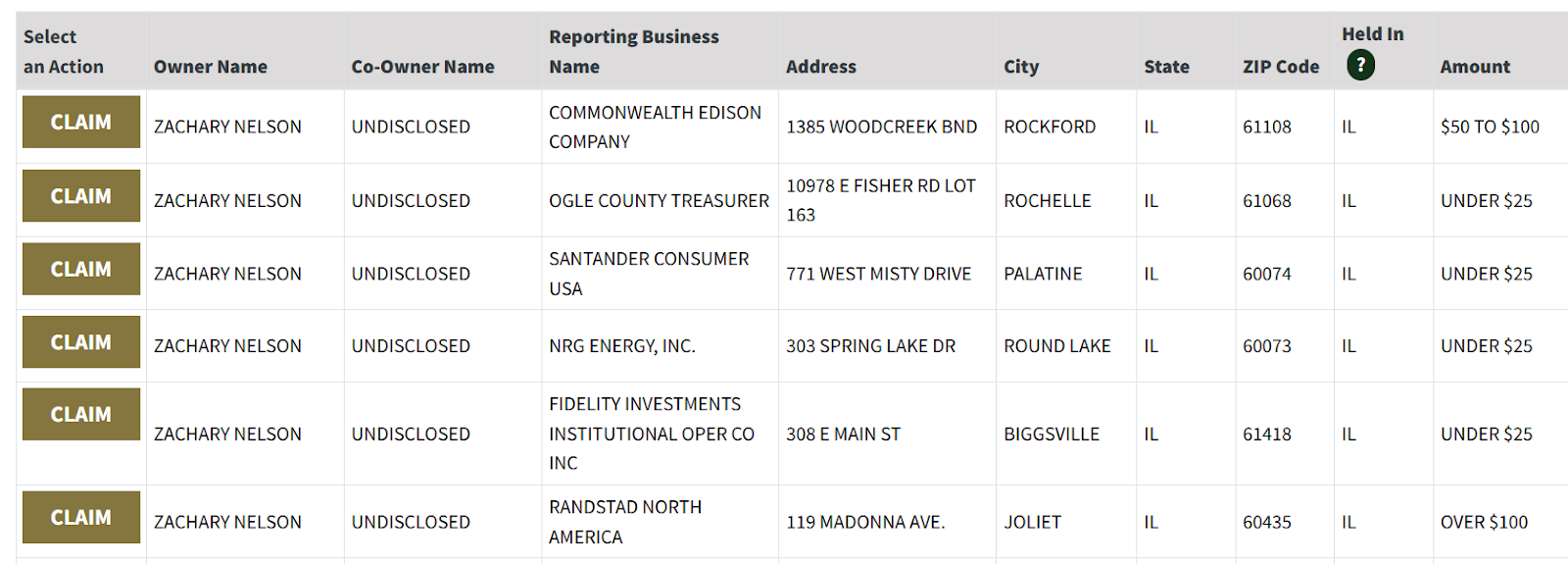

6. Check for Unclaimed Money

You ever forget some money in your coat pocket, only to find it again next winter when you wear the coat again?

Well, the government has a giant winter coat, and its pockets are stuffed with billions of dollars people have forgotten about.

And that money sits there every year, waiting for people to go through the pockets and find their lost money.

So far, this sounds like a scam, right?

I promise it’s true, a Nigerian prince told me about it.

But also, it actually is legit.

None of these are me. But if they were, I could claim it in a few minutes.

When a business tries to send you money and can’t find you, they give that money to the State Treasurer to hold.

Like a giant lost & found full of money.

This money is usually things like

Forgotten savings accounts

Uncashed checks

Utility refunds

Final paystubs

Abandoned stock holdings

Even physical gold from deposit boxes

Give it a shot (and check the names of relatives too), I’ve found hundreds of dollars for people this way.

How to Check:

Visit Unclaimed.org (official website for all states) or MissingMoney.com.

Search under your current and previous addresses.

Advanced

7. Open a Donor-Advised Fund (DAF)

A DAF is an investment account for charitable giving.

People like them for 3 reasons

Tax planning around charitable giving

Avoiding taxes on investments that have gone up in value

Investing your charitable funds into impact-making for-profit companies

And you don’t have to be a mega-gajillionaire to create one.

Most require only a couple hundred dollars to get started.

(There are tax benefits and drawbacks not mentioned. Talk to an advisor before opening one.)

1. Tax planning around charitable giving

A DAF allows you to fill it with money now that you'll give away later, while getting the tax write-off right away.

This lets you supercharge your tax deductions from giving into a single tax year.

For example - you could put all your planned donations for 2025 into a DAF this year.

Then during the upcoming year, you can use your DAF to meter out your donations as you like.

Doing this, you’ll get to deduct all of that giving in 2024 (big tax savings).

Then you take the standard deduction for your income taxes in 2025.

This way you don't have to clear the standard deduction in both 2024 & 2025 before itemizing your giving.

Making more of your giving tax-deductible.

2. Avoiding taxes on investments that have gone up in value

If you own stocks that have gone up in value, you can donate them to the DAF.

The DAF is a charity, so it doesn't pay taxes on their growth.

That can give you a huge capital gains tax savings (and boosted giving).

3. Investing your charitable funds into impact-making for-profit companies

DAFs also allow you to invest your money while you wait to donate it. (pretty awesome)

You can do this in a regular index fund.

Or you can use it to invest in for-profit companies that also are doing good in the world.

For example - invest it in a water purification company in Haiti.

Or in a job-training company for convicted felons in Chicago.

Your money does good now, while growing so that it can go do more good again in the future.

How to Start: Providers like Fidelity Charitable or Schwab Charitable make opening a DAF easy. I also have friends who like the National Christian Foundation and the Impact Foundation because of the positive investment opportunities they offer.

Pro Tip: DAFs are particularly valuable if you’re in a high-income year and want to maximize your tax benefits.

8. Do a Roth Conversion

If you think your income this year will be lower than in future years, this move could be smart.

A Roth conversion takes funds in your traditional IRA and converts them to a Roth IRA.

This triggers taxes (but not penalties) on the money you convert (as if you had earned that money as income this year).

This allows you to lock your taxes to a lower tax bracket now and never pay taxes on that money again.

Bonus: If you live in Illinois like I do, you might not even pay state income taxes on that conversion. Which gives you a bonus tax win.

Why Do It Now: If your income is lower this year, your tax liability on the conversion will also be lower.

How to Do It:

Contact your IRA provider to start the conversion.

Work with a tax advisor to calculate the tax implications.

Pro Tip: Avoid converting too much at once to stay within a lower tax bracket.

9. Negotiate a Raise or Promotion

Many companies do year-end performance reviews in December and January.

That makes it the perfect time to begin the process of asking for a raise.

Don’t just walk into your performance review meeting guns blazing though.

Try this instead:

“Hey boss, thanks for the great feedback for this year.

I’m excited for what’s coming in 2025.

Also, I’d love to sit down with you sometime soon to talk about what it would take to earn a (promotion/raise)?”

Then leave space for them to speak.

This isn’t the time to ask for the raise, this is the time to set up the conversation about one.

If you want a recording of a 1-hour workshop where I broke down exactly how to ask for a raise, reply back to this email and I’ll send it to you.

How to Prepare:

Whew!

That was a lot to dump on you at once.

And the risk with that is leaving you with so much to think about that you never actually use the information.

I don’t want that to be you.

If you want to win (and not just feel like you’re winning), choose 1-2 of these to take action on TODAY.

Your future self is waiting. Betting on you.

Let’s hit 2025 strong.

Keep growing,

What’d you think of this week’s newsletter? Hit reply to let me know!

Forwarded this email? Subscribe here